/Website/Global%20Assets/navigation/IR_Case-Study-Top-IMB%20(1).png)

/Website/Global%20Assets/navigation/IR_Blog--Stay-Ahead-of-Trigger-Lead-Reform-op1.png)

/Website/Global%20Assets/navigation/IR_Announcement_2026-HW-Tech100-Mortgage-Winner2.png)

How Informative Research Is Helping Lenders Prepare for the Trigger Lead Changes

With the trigger lead bill, the Homebuyers Privacy Protection Act (HPPA), set to reshape how credit inquiries can be used, lenders are preparing for...

The Fair Credit Reporting Act is a federal law that regulates how credit reporting agencies collect data about individual consumers and how they share that data. This law helps keep credit reporting agencies, banks, and lenders accountable for how they use credit information. Keeping consumer information lawfully private and protected is much like securing a civilian's medical or school records. The protection this act provides is a significant benefit for individual consumers.

In this guide, we'll go over:

In 1970, the FCRA was created primarily for the three major credit reporting agencies: Experian, Equifax, & TransUnion. These three credit agencies are all private companies but regulated by federal (and sometimes state) agencies because of the information they collect and how they sell it. The Federal Trade Commission (FTC) and the Consumer Financial Protection Bureau (CFPB) are the federal agencies that oversee and enforce provisions of the act. The CFPB serves as a consumer watchdog in the financial industry. "The CFPB was created to provide a single point of accountability for enforcing federal consumer financial laws and protecting consumers in the financial marketplace. Before, that responsibility was divided among several agencies. Today, it's our primary focus." According to the CFPB's website statement. These agencies provide oversight to financial companies that otherwise could have significant power over consumers. This is important because a credit profile based on inaccurate data can follow a consumer for years and cloud every financial decision they make.

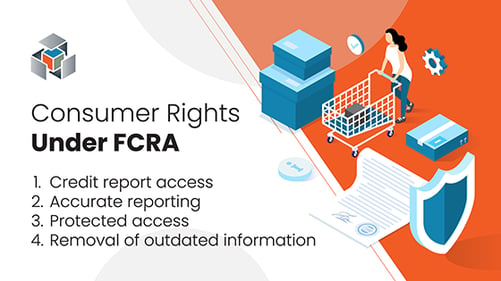

The FCRA official document is massively long and goes into great detail, but essentially, there are four major rights that consumers have under the FCRA. Let's go over each one in more detail.

1. Credit Report Access

The first protected right under the act is that a consumer, with proper identification, is allowed access to their credit file, once a year, for free. This is different from any other credit reporting service. If requested, the three credit bureaus must provide all the information they've collected without negatively impacting the consumer's credit score. This right also specifies what kind of information the bureaus can collect. This includes bill payment history, past loans, and current debts. Bureaus may also have employment status, previous or current addresses, files for bankruptcies, owed child support payments, and even arrest records. The purpose of this right is to give access to the consumer's own individual credit profile. For example, when potential borrowers know whether their credit profile is in good standing, they feel more confident applying for a mortgage loan. This also lets them see what information has been reported and ensure that it is correct.

2. Accurate Reporting

Another important right is Accurate Reporting. Since the act allows consumers to look at their credit profiles for free, they can also check for inaccurate information. Inaccurate information can do much more than just affect a credit score or loan application- inaccuracies can be a sign of fraud. Accurate Reporting gives the consumer the right to dispute any incorrect information. The consumer reporting agency must verify if that information is erroneous and change or remove it. If the consumer cannot resolve the inaccuracy, they can add a statement to their profile explaining the situation.

3. Protected Access

The FCRA also protects consumers' credit files by limiting access and requiring consumers' consent in certain situations before access to the consumer's data is allowed. Consumers also have a right to see who has accessed their files within the last year and within the previous two years for employer-related inquiries. They even get notified if it has been used against them in any way. Reporting agencies are only allowed to share data with those identified as having a "permissible purpose." This is given to companies like lenders, any current creditors, and cases of court-ordered access. Protected access also allows the consumer to freeze their credit for protection in the case of fraudulent activity or identity theft.

4. Removal of Outdated Information

Arguably, the most vital right the consumer has is the obligation of credit reporting agencies to remove certain information. Negative information must be removed after seven years, and bankruptcy filings are removed after ten years. However, criminal records may remain indefinitely. This allows consumers to repair their negative information, so it doesn't harm financial opportunities for the rest of their life.

Since the FCRA establishes rights for consumers that require credit reporting agencies to do their due diligence, these laws and regulations need to be enforced. If a credit reporting agency is found in violation, there are severe penalties. The FCRA also requires that a lender, insurer, landlord, employer, or anybody else seeking somebody's credit report, have a legally permissible purpose of obtaining the report, which means if obtained illegally or used illegally, there are also penalties. Each violation may carry a fine of between $100 and $1,000 as well as punitive damages without factoring in how much one would have to pay for an attorney. If someone knowingly uses the information under false pretenses, that person could incur criminal charges.

Additionally, this act holds lenders accountable for denied credit applications, especially if discrimination is involved. These laws are set in place because a lender must have a substantial reason based only on a credit file's information. Consumers have the right to know why they've been denied credit based on what their credit file contains. Lenders who violate these laws harm their careers, their companies, and especially their clients.

It's no secret that accurate credit information is vital in the financial industry. That's why consumers' credit information should not be a secret. Under the FCRA, credit reporting agencies work to report and share accurate information, which helps consumers understand their credit potential and allows lenders to access that credit potential. The FTC and CFPB are working to ensure that the financial industry is transparent with consumers' information by enforcing the laws and practices that hold lenders and lending companies accountable. Borrowers are more inclined to borrow when they know they have rights and recourse in situations where they are denied credit, get their identity stolen, or have other problems with their credit file. The FCRA helps the CFPB promote a more transparent, accessible, and accurate credit reporting system.

/Blogs/2026%20Blogs/03-26-Trigger%20Leads/IR_Blog--Stay-Ahead-of-Trigger-Lead-Reform-op1.png)

With the trigger lead bill, the Homebuyers Privacy Protection Act (HPPA), set to reshape how credit inquiries can be used, lenders are preparing for...

/Blogs/2026%20Blogs/03-26-Trigger%20Leads/IR_Blog--Trigger-Leads-Are-Changing.png)

Trigger leads have been a point of frustration for borrowers and lenders for many years. With the recent passage of the new trigger lead bill , the...

/Blogs/2026%20Blogs/02-26-TWN%20Indicator/IR_Blog--Income-Qualify-and-The-Work-Number-Report.png)

Mortgage teams don’t just need data. They need certainty early so they can route loans correctly, avoid unnecessary verification steps, and keep...