/Website/Global%20Assets/navigation/IR_Case-Study-Top-IMB%20(1).png)

/Website/Global%20Assets/navigation/IR_Blog--Stay-Ahead-of-Trigger-Lead-Reform-op1.png)

/Website/Global%20Assets/navigation/IR_Announcement_2026-HW-Tech100-Mortgage-Winner2.png)

How Informative Research Is Helping Lenders Prepare for the Trigger Lead Changes

With the trigger lead bill, the Homebuyers Privacy Protection Act (HPPA), set to reshape how credit inquiries can be used, lenders are preparing for...

.jpg)

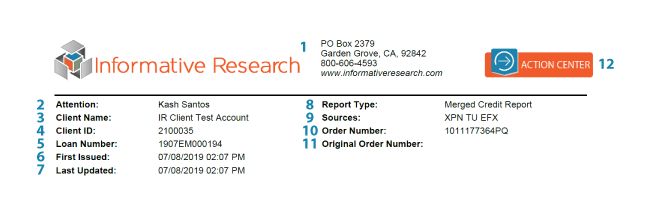

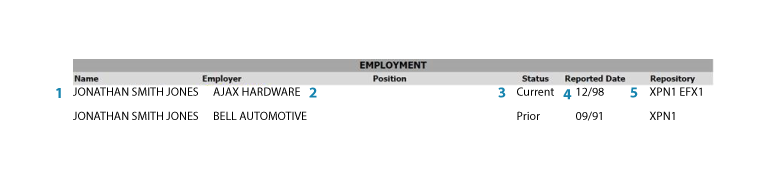

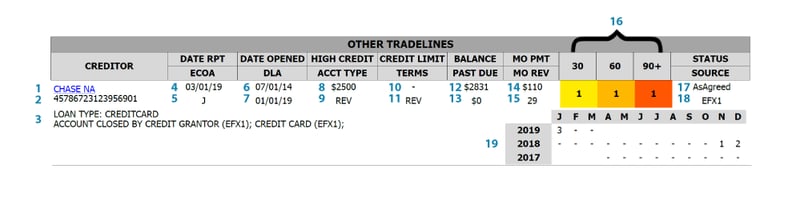

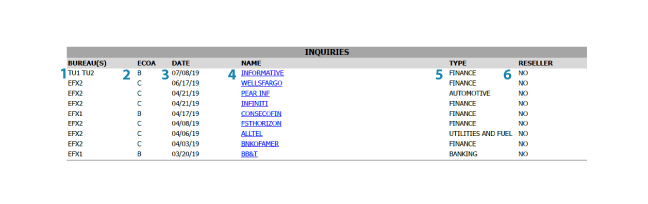

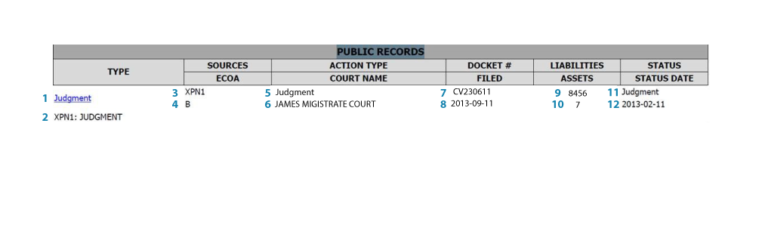

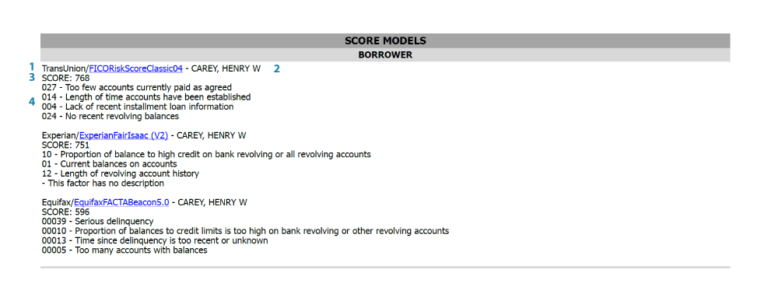

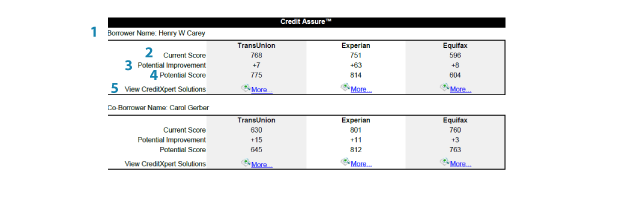

Credit reports aren't the easiest piece of information to read and it's a layout that the industry isn't going to revamp any time soon.

Luckily, our credit reports are designed to be simple to review and interpret. We've accumulated numerous formats because we continue to create custom layouts that fit our client’s unique needs (because every partner is different).

Because each credit report contains a vast amount of data we can separate sections and customize their order within a report so your underwriters can make informed lending decisions more efficiently. Our credit reports can be ordered on Web Credit System or through your LOS. For our current LOS Integration Status please email info@informativeresearch.com.

Learn more about the different report sections by clicking on the title:

1. Name, address, website, and phone number for all three credit bureaus

/Blogs/2026%20Blogs/03-26-Trigger%20Leads/IR_Blog--Stay-Ahead-of-Trigger-Lead-Reform-op1.png)

With the trigger lead bill, the Homebuyers Privacy Protection Act (HPPA), set to reshape how credit inquiries can be used, lenders are preparing for...

/Blogs/2026%20Blogs/03-26-Trigger%20Leads/IR_Blog--Trigger-Leads-Are-Changing.png)

Trigger leads have been a point of frustration for borrowers and lenders for many years. With the recent passage of the new trigger lead bill , the...

/Blogs/2026%20Blogs/02-26-TWN%20Indicator/IR_Blog--Income-Qualify-and-The-Work-Number-Report.png)

Mortgage teams don’t just need data. They need certainty early so they can route loans correctly, avoid unnecessary verification steps, and keep...